SpaceX Could Get Dangerously Systemic

Options could drive its valuation to a point that exposes our capital markets as permanently broken.

“It’s just going to get

Weirder and weirder

And weirder and weirder

And finally

It’s going to be so weird

That people are going to have to talk about

How weird it is”

— Terence McKenna

For years I’ve been asking how weird things have to get before we admit the stock market is outright fundamentally broken. After watching SpaceX surge after hours today, I think the answer is obvious: the market is already broken. The real question is how much more absurd things need to get before everyone else notices.

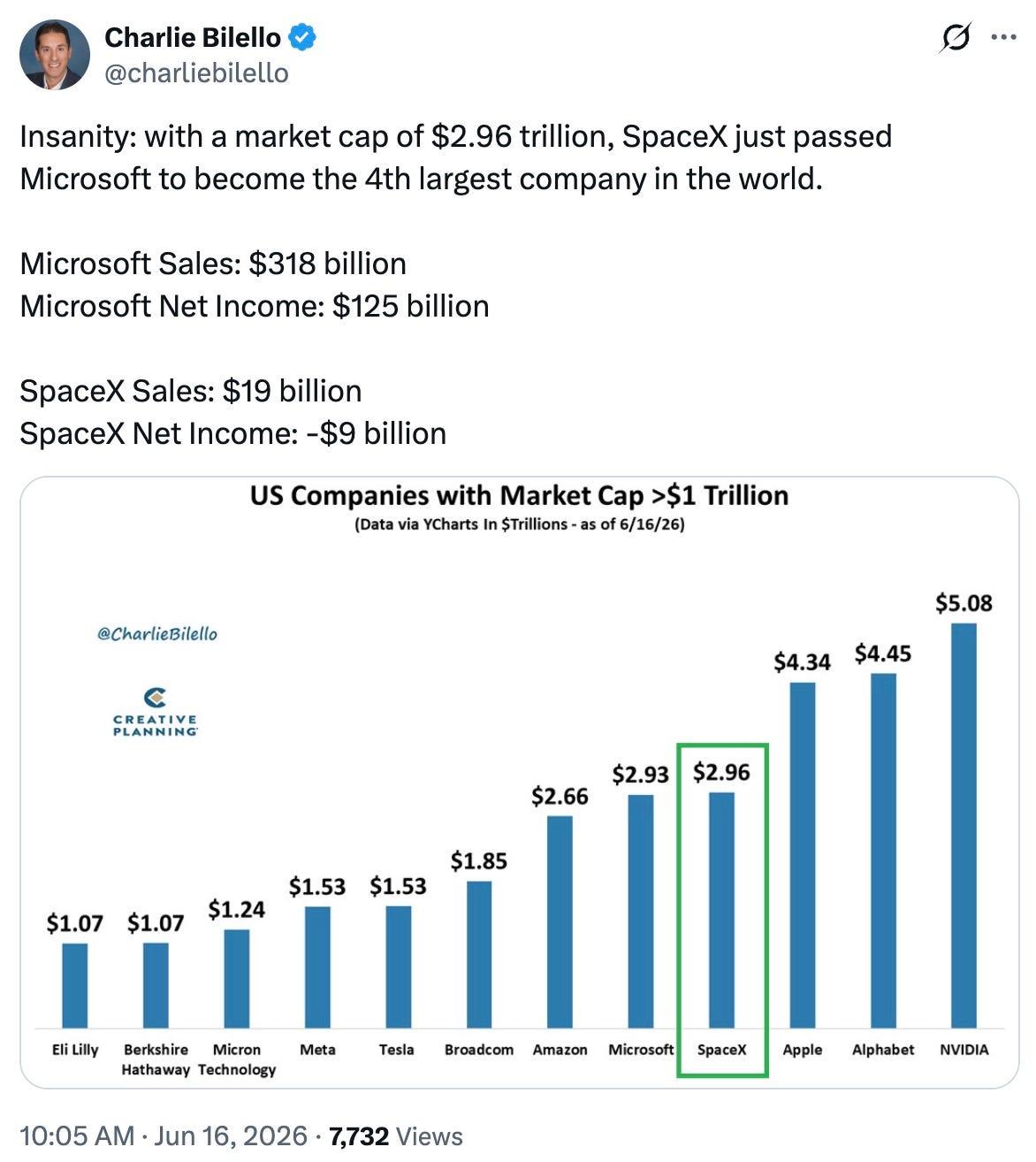

SpaceX crossed above $3 trillion in market cap in after-hours trading. That makes it worth more than Amazon and Microsoft.

Microsoft generates hundreds of billions of dollars in annual revenue and well over $100 billion in annual profit.Amazon generates more than $700 billion in annual revenue and tens of billions in annual profit.

SpaceX is now being assigned a higher valuation than both.

SpaceX’s relatively limited float makes it an ideal candidate for manipulation squeeze dynamics. Near the close of after-hours trading, the stock had briefly approached $230 per share. In a single day, roughly $650 billion of market capitalization was created for a company losing billions of dollars a year.

$650 billion. Not over a year. Not over a decade. In a single day. And tomorrow options begin trading, and as I’ve predicted, I’d bet it’s going to squeeze harder.

That’s the part that should make everyone uncomfortable. Because I’ve spent years writing about what happens when options activity becomes the primary driver of price action.

We’ve already seen the playbook: call buyers show up, dealers hedge, the stock rises, momentum traders chase, more calls get purchased and the cycle repeats.

Update 6/16/26: As of 1030AM EST on its first day of options trading, more than 500,000 contracts, representing a notional 50,000,000 shares have traded.

The $380 strike call expiring in two days — the furthest out of the money strike available to buy — is the second most popular strike in the weekly call options and was the leading strike in early trading.

At some point, price stops measuring value and starts creating value. The valuation itself becomes the bullish thesis. The company’s industry and its fundamentals become totally meaningless. And you officially have a market doing the opposite of what it should be doing.

And that’s why tomorrow matters. Because options begin trading on a company that has already demonstrated extraordinary squeeze dynamics. And so has its sister company.

I’ve been writing for years that modern markets are increasingly driven by mechanical forces rather than fundamental analysis. Tomorrow may provide one of the clearest demonstrations of that thesis yet.

My expectation is that the introduction of options trading in SPCX will not improve price discovery. It will further distort it. If aggressive call buying emerges, dealer hedging activity could create the same type of reflexive feedback loops that drove some of the most spectacular (and totally nonsensical) moves in Tesla and other momentum names over the last decade.

At that point, price movement has nothing to do with business fundamentals and everything to do with market structure. And if SpaceX experiences the type of gamma squeeze that many traders are openly anticipating, I believe it will strengthen the case that modern markets are useless…and extremely dangerous to the average retirement account.

Because markets are supposed to allocate capital and are supposed to facilitate price discovery. They are supposed to connect valuation, however imperfectly, to economic reality. They are not supposed to function as self-reinforcing feedback machines capable of adding hundreds of billions or even trillions of dollars in market capitalization through mechanical flows.

The question is not whether SpaceX is a good company. The question is whether the market structure surrounding it is healthy.

Because if a company can become worth more than Microsoft and Amazon (and tomorrow probably Nvidia) despite producing only a fraction of their revenues and earnings, what exactly is the limiting factor? What stops this from becoming a $5 trillion company? A $10 trillion company?

Because if the same options-driven feedback loops that propelled Tesla after late 2019 emerge here, those numbers are no longer as unimaginable as they once seemed. And that’s what nobody seems willing to discuss.

Everyone wants to talk about how high SpaceX can go. Nobody wants to talk about what happens if it gets there.

At $10 trillion, we’d be talking about a company worth roughly one-third of U.S. GDP. A company so large that it would dominate passive indexes, retirement accounts, ETFs, pension funds, and institutional portfolios. A company whose rise and fall would increasingly dictate the behavior of the entire market…while not even being profitable. It would be the greatest and most dangerous hype machine ever built in the history of mankind.

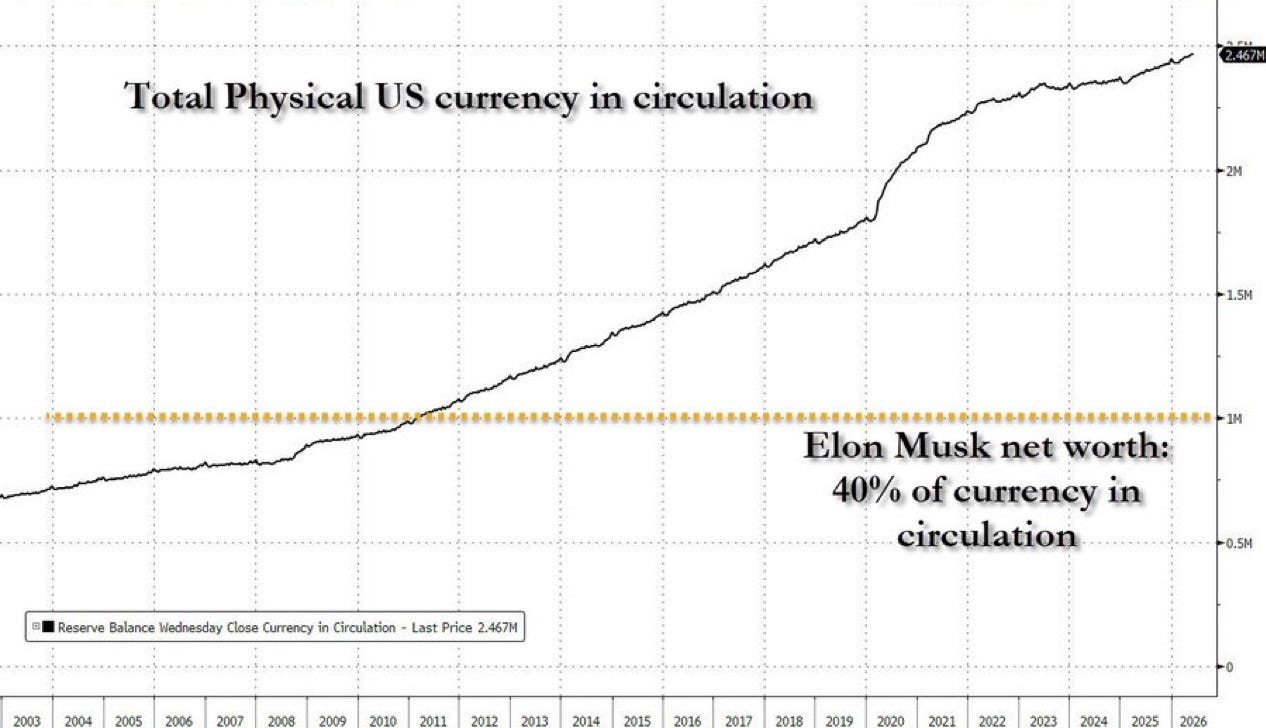

And consider what that would mean for Elon Musk. At a $10 trillion valuation, Musk’s personal fortune would move into territory that has no precedent in modern history. His net worth is already 40% of all currency in circulation.

Source: Zero Hedge

And he’s not just richer than the second-richest person. He could soon be something like ten times richer than the second richest person.

The gap between Musk and the rest of the billionaire class could become larger than the fortunes of entire first world nations.

At that point we aren’t talking about ordinary wealth creation anymore.

What happens if SpaceX’s market cap somehow reaches $28 trillion on a gamma squeeze glitch? That’s roughly equivalent to the annual economic output of the United States. Would people finally start questioning the market then, or would they simply find new ways to rationalize it?

Because that’s what every bubble in history has done. Every new high becomes proof that the previous high was too low. Every speculative mania becomes innovation, just ask “expert” on innovation Cathie Wood. Every squeeze becomes genius. Every warning becomes evidence that the skeptics just don’t understand the future.

The most remarkable thing about SpaceX crossing $3 trillion isn’t the valuation itself.

It’s that if this continues it’ll get too big to ignore and at some point we’ll have to stop debating SpaceX and start debating the system that produced it: a speculative machine that has become completely untethered from its original purpose.

The danger is that once a company reaches sufficient scale, the distortion itself becomes systemic. Every passive fund has to own it. Every major index becomes dependent on it. Pension funds, retirement accounts, sovereign wealth funds, insurance companies and institutional portfolios all become increasingly exposed to the same trade. The higher it goes, the more unavoidable it becomes.

And that’s the part that nobody seems to understand. If SpaceX eventually reaches $10 trillion through a combination of hype, narrative, mechanical flows and options-driven feedback loops, it won’t just be a SpaceX story anymore. It will become the market. Its movements will increasingly dictate the performance of indexes, ETFs and retirement accounts across the entire financial system. The market will effectively become a referendum on a single stock.

That’s how bubbles become systemic. Not when they’re small enough to laugh at, but when they become so large that everyone is forced to participate. The same mechanisms pushing prices higher today eventually create the conditions for instability tomorrow. When trillions of dollars of wealth become tied to a valuation that was never anchored to fundamentals in the first place, even a modest reversal can have consequences far beyond the stock itself.

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions.

As of May 20, 2026 I personally no longer actively trade (read my story here). My investing/saving is done by recurring contributions mostly to sector ETFs and a few select equities, trusted third parties who oversee my accounts, and advisors. Such advisors or funds, through individual equities, options, index funds, mutual funds, ETFs, or other securities, may have positions in, exposure to, or holdings of names mentioned herein that I know nothing about. Basically, via index funds, ETFs and individual equities it is possible I could own, have exposure to, or not own anything at any point. As of the same date, May 20, 2026, in an attempt to lead a healthier lifestyle, I’ve also excluded myself from fantasy sports, sports betting, online and in-person casinos and prediction markets.

And all positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

I don’t know, Chris, but your recent writings have been spot-on fire…not that your previous articles didn’t have the same punch…it’s just - different…and it feels more prescient…

forget dot-com…we’re in tulip territory now…

One of the nice things about getting old Chris (I’m mid Gen X) js you learn there is little you can do about people’s stupidity.

Think of it this way. Anyone too young to have experienced 2000 and 2008 (I exclude 2020 because it was an exogenous shock) has decades to recover from the upcoming mess.

Anyone who did experience 2000 and 2008 should know to insulate their portfolio from the coming madness. If you are too lazy or greedy to do so, hard to have sympathy for you. It doesn’t take much time or brains to put your 401 K in a targeted retirement fund that will automatically reduce your exposure to equities as you get close to retirement.