This Financial Crisis Will Be Like None Other In History

Here's how I think it goes down.

It looks as though Credit Suisse is going to be sold off for pennies on the dollar, temporarily postponing a financial trainwreck, at least for a couple more hours or days, until the next shoe inevitably drops.

The Fed doesn’t seem keen to wait. U.S. dollar swap lines are being used to “enhance liquidity” and the Central Bank has all but thrown in the towel on the tightening cycle, it appears.

In response to the news and at the time of this writing, about 3:30AM EST, equity futures are mixed after being higher immediately after opening on Sunday night.

It’s tough to solidify exactly what’s going happen in the short term with U.S. markets, especially with things changing by the hour. But there are two things that I think are worth solidifying about the conundrum markets and the Federal Reserve find themselves in now.

The first is that this crisis isn’t going away anytime soon - it may shape-shift, but it’s not going away. The second is that the outcome of this crisis is going to be unlike anything that’s ever occurred in history.

Even though Central Bank bailouts look as though they’re going to be ubiquitous in coming weeks (as we’re already seeing with the Fed and the Swiss National Bank), it doesn’t mean that the crisis isn’t going to persist in another form.

These blowups in the system are zero sum games. Stop them from erupting through one manhole cover, and they have to eventually find another one to blow open.

When Central Banks all over the world bail out their respective institutions and equity markets, many will think it’s just been another crisis…and another crisis averted.

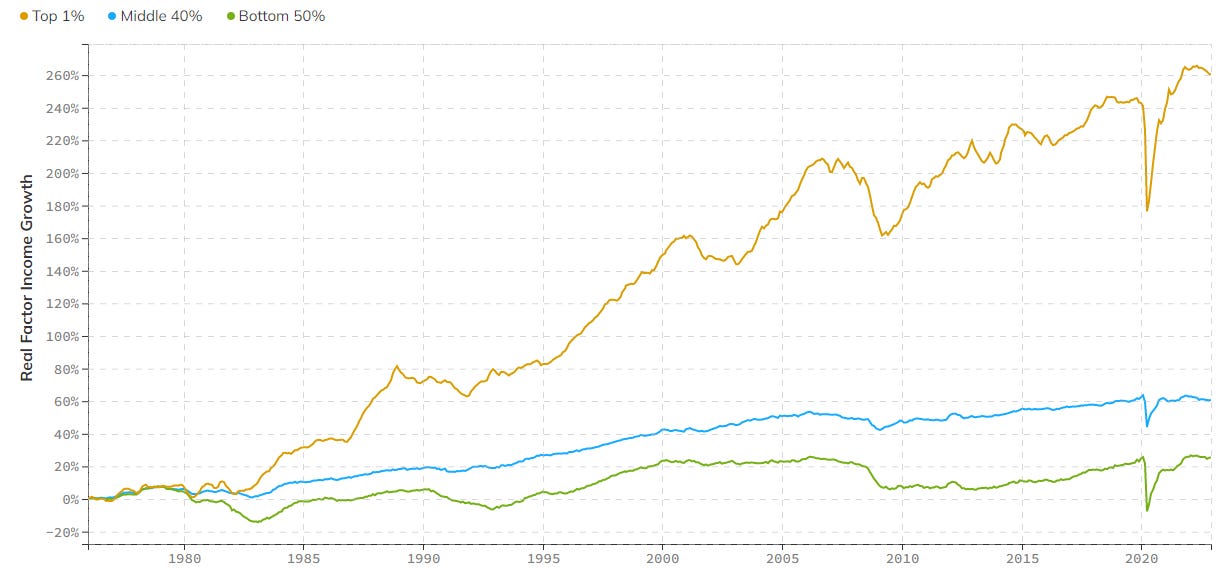

The usual Austrian “crazies” will prattle on about moral hazard, the wealth divide will get even wider, there will be “Occupy”-style protests again…but life will go on.

“Ho hum,” most market participants will say to themselves, content that another SuperSized™ bag of dogshit didn’t hit the fan during their lifetime and will instead be bequeathed unto their grandchildren at about the same point the U.S. dollar has the global appeal of a moldy Kraft Single™ cheese slice that’s been sitting out in the sun for 5 weeks straight.

But that lot has another thing coming this go-round, if you ask me. This time, the crisis truly is different because of the geopolitical setup.

As I have written about extensively over the last year, the global economy is dividing into two. On one hand, you have the West and our printing-press-based Central Banking policies. On the other hand, you have a growing constituency born out of a maturing Russian and Chinese alliance, now also inclusive of India, Saudi Arabia, and other nations. The petrodollar is dead, China and Russia are openly hoarding gold and some fund managers believe that Xi and Putin know that the West is running a ponzi scheme.

For a recent primer on just how the global economy is shifting, I’ll once again recommend this exceptional February 2023 interview with Andy Schectman, who lays out the global landscape in surgical detail, in less than an hour.

Andy lays out the thesis “that the world is poised for a monetary reset which would result in the BRICS having their own reserve currency, likely backed by gold, and how this goes hand-in-hand with de-dollarization trends that are currently unfolding”.

The important thing to realize when thinking about our current “crisis” is that this unprecedented setup globally that Andy describes very well will likely lead to an unexpected and unprecedented result.

People need to understand that the Fed can’t stop what has already been put into motion. Market psychology has broken, as I noted last week several times, and risk aversion is now front and center. The Fed has capitulated, as Zero Hedge accurately noted last night:

But no matter what the Fed does now, it’s going to be on a lag. This means they can’t just cut rates tomorrow and have the problem fixed by Wednesday. They’re now in a “dead zone” where the seeds for the next several months have already been sown no matter what action they take with rates.

I have guessed that the blowups we are seeing now are result of rate hikes that took place last year. That means that the consequences of current rates won’t be felt for another several quarters to come.

Silicon Valley Bank blew up because it was reaching for bonds when yields were near 1.5%. Their portfolio likely started to sustain serious damage as soon as rates were hiked from that level. If you don’t think other funds were taking similar bets, including continuing to buy bonds as yields became more attractive, you’re crazy.

This means that as the Fed “stayed the course” the last 12 months, others likely suffered similar-style losses as SVB’s. We just haven’t heard about them yet.

Rate expectations are moving lower now, but it’s too little too late for others whose fates have been sealed already, in my opinion. We may hear about these names in coming days.

Putting aside that this crisis will almost certainly be used to usher in a Central Bank digital currency, one could mistakenly believe that money printing will once again get everything “under control”.

But instead of that being the case this time, what if the BRICS nations use this crisis as an opportunity to challenge the Western Central Banking empire? All I’ve been writing about for the last year and a half is how central banks in places like Russia and China have been stockpiling gold.

There’s no point in doing this unless you eventually feel as though, to some degree, you’re going to have to fall back on gold as a baseline or a safeguard.

And a financial crisis is the point where people lose their faith in the existing system the most, thereby making it vulnerable to be usurped, if not practically at least psychologically. That makes a strong argument for (1) bitcoin perhaps either gaining traction or upsetting regulators enough to draw more ire right now and (2) the BRICS nations seeing this as an opportune time to try and challenge the U.S. dollar openly.

The pieces have already been put into place. The timing has never looked better:

Lest we forget that inflation continues to run rampantly out of control. Last year I was asking whether or not we would endure inflation or a recession, arguing that we would have to deal with one or the other due to the Fed raising rates.

It has now become clear that the central banks of the west are going to surrender to inflation. The idea of easing and trying to manage this crisis with inflation as high as it already is sets the table for the longshot hyperinflationary scenario that many people laughed at over the last year. I’m not saying it’s definitely going to happen, but I’m saying that the setup is making it look more like a possibility than ever.

As is a function of Keynesian theory, bubbles get bigger and bigger as we kick the can down the road. This means that bailouts also get bigger and bigger as we kick the can down the road. Eventually, at some point, we lose control and some economic variables (like gold and M2) go into an unstoppable parabolic spike upward while others (like, perhaps, equities) go into a dead engine stall.

To be honest, for the long-term, it’s difficult to forecast whether or not current policy will result in U.S. markets moving drastically higher on a nominal basis, or whether they will simply wind up like Japan, treading water for years to come as the Fed expands QE into every asset that isn’t nailed down.

It also remains difficult to try to forecast what’s going to happen in the short term. My guess is that equities are going to crash before eventually catching a bid once the lag of central bank panic being put into place today passes by, over the next year or so.

When the smoke clears, who knows what the situation looks like. We will have moved one iteration further into an alternate euphoric Keynesian reality than we were in March 2020, which seems impossible. Will the NASDAQ trade at a 60x multiple? Will the dollar index be at 40? Is there even a case where the US dollar holds up here and remains global reserve currency? It’s difficult to foresee, but that doesn’t make it an impossibility.

In addition to inflation, we also have to be acutely aware that there is a very real chance that war drums beat louder over the next year.

China moving into Taiwan is a real risk and we are already fighting a war against Russia via proxy in Ukraine. As China moves closer to Russia in supporting them and the US moves closer to Ukraine, the stage is set not just economically, but also militarily: the west and NATO are at war with Russia, China, and soon to be the nations they are supported by, like India and Saudi Arabia.

This war will not just be militarily, it will be over the fate of the new global reserve currency as well.

From CNN:

Chinese leader Xi Jinping will fly to Moscow next week to meet with President Vladimir Putin in his first visit to Russia since Putin launched his devastating invasion of Ukraine more than a year ago.

The visit will be seen as a powerful show of Beijing’s support for Moscow in Western capitals, where leaders have grown increasingly wary of the two nations’ deepening partnership as war rages in Europe.

It will also be Xi’s first foreign trip since securing an unprecedented third term as president at the annual meeting of China’s rubber-stamp legislature last week.

The face to face was revealed on Friday by statements from both Beijing and the Kremlin.

Now, a look at how I’m positioned and what I continue to buy and own.