The Soft Landing Charade

If you believe we're in for a soft landing, I have some unprofitable tech companies trading at 200x sales to sell you.

It is of the utmost importance that my readers know I am capable of being bullish.

I always find it necessary to repeat this, over and over, when I feel like I am droning on about what I believe to be a forthcoming, looming bearish scenario. There are tons of people out there claiming stocks are going to crash 90% and never recover, and I’m just not in that camp. But that’s not to say I’m not totally cautious on markets right now.

You can lump me in with doomsday sayers, conspiracy theorists and total hack financial newsletter writers if you want. I don’t mind. Hell, nowadays, I take that as a compliment. But if one thing sets me apart from many other “permabears”, it’s the fact that I have been bullish and I will be bullish again. And I genuinely feel understood by most of my readers.

To quote Grace from Ferris Bueller’s Day Off:

“The sportos, the motorheads, geeks, sluts, bloods, wastoids, dweebies, dickheads - they all adore him. They think he's a righteous dude.”

So thanks for that.

One instance where I was both bearish and then bullish was in 2020, when Covid was newsworthy enough to be right in front of our faces, but wasn’t being touted by U.S. media enough to induce panic just yet.

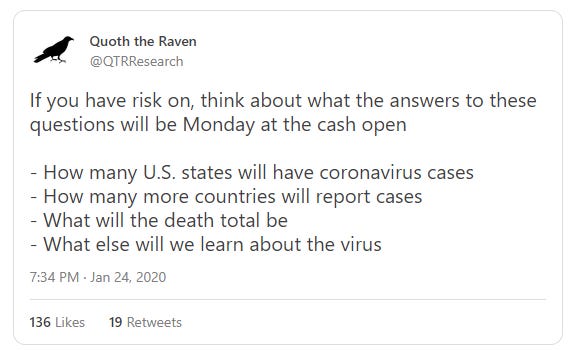

On January 24, 2020, with the Dow at 29,230, I warned that the stock market was “not pricing in any type of event involving this coronavirus spreading across the U.S.” and that the market was “extraordinarily overpriced relative to near-term risk”.

I also urged people to consider how many U.S. states would eventually have cases, how many more countries would have cases and what else we will learn about the virus.

On February 2, 2020, I noted via tweet that people were starting to use the word “pandemic” to describe the coronavirus and say:

“I take zero pleasure in this but I think a serious wake up call is coming for some asset managers. And is long overdue. Just my opinion.”.

The World Health Organization doesn’t declare the coronavirus a pandemic for another 38 days. Later in February, I wrote:

“The world’s second largest economy is shut down amidst an epidemic/pandemic that we have questionable details about - and the market can’t stop scorching to new highs.”

On Februrary 20, 2020, with the Dow at 29,296, I again warned there was a “wake up call for those ignoring virus impact coming”, that the market was underpricing risk due to the virus and that “pain is coming”.

The Dow would drop more than 30% in coming weeks to a 52-week low of 18,213.

Shortly thereafter, on March 11, 2020, I appeared on Jon Najarian’s podcast where he asked whether or not the market had finally capitulated in reacting to the emerging pandemic. We talk about the difference between being a permabear and being a skeptic based on common sense.

“I don’t think we have systemic financial risk now,” I say when asked about the state of the macroeconomic as a result of the developing pandemic.

I talk about why I am overweight gold and silver and plan on continuing to be overweight precious metals. Gold was about $1,689 at the time.

“I don’t think we’ve seen capitulation yet. We don’t really know what the long-term impact of this recession, and more importantly the Fed’s response to it, is going to be. We could turn into Japan as a result of this,” I say.

The VIX was at 53 on the day the podcast was recorded.

Two days later, on a day the Dow falls 10%, I start coming around to the idea that the virus isn’t going to be devastating enough to stand in the way of what the Fed is doing with QE infinity.

I tweet that “there's a chance the tailwind coming out of the coronavirus WAY down the line, with 0% rates, discount window open, short sell ban, etc. could be ungodly.”

12 days later Bill Ackman says “hell is coming” live on CNBC and the market bottoms, the S&P closes at 2,447.

One year later, the S&P would fly through 4,000.

In May, I continued my bullish thoughts and talked to George Gammon about market direction going forward, joking about how Jim Cramer was telling people to sell their index funds and how Warren Buffett was claiming he had been priced out of the market by the Fed.

“I almost find this as a contrarian indicator. I wouldn’t be surprised if the market goes straight up now. Just because Buffett’s been priced out of the market and doesn’t see value doesn’t mean that this crazy psychotic tailwind of stimulus isn’t going to continue to drive the market higher.

First day after Cramer says that. Dow’s up 400 points. Something to have fun with. I just found it pathetic that people cling to Buffett’s narrative like it’s the end all be all. He gets things wrong. He was in the airlines, they just got clobbered. It’s possible for him to get things wrong.”

By August 2020, I was full-on bullish. With the S&P at 3294 and the Dow at 26,664 , I appeared on Seeking Alpha’s Alpha Trader podcast and said:

“I feel like the S&P is going to go over 4,000 next year,” I tell the hosts. “The market is basically sipping on rocket fuel that the Fed is giving it.”

“Remember, every single person in March and April that went on CNBC said ‘we have to retest the lows’ and ‘we have to go back to Dow 17,000’. Gundlach said it, everyone said it. I’m the only person who didn’t say it and said we could just launch from here.”

“I’m long equities and I’m long gold and silver,” I said.

With regard to the reaction to Covid, I say: “Over the next 6, 12, 18 months I think we’re gonna look back and say ‘OK, we may have overreacted a little bit. I think we have a lot of tailwinds. I think we are going to have one good vaccine and therapeutic headline after another from now until next summer.”

The point here isn’t to take a victory lap, go full Barry Horowitz and spend this article patting myself on the back. The point is to show you that I have the capability of being bullish, yet I am still extremely bearish on both equities and the economy right now.

Just as Buddhists say things like “there is no light without darkness” and “there is no day without night”, I’ll add “there is no being furiously bearish without, at some point, being bullish”.

With that out of the way, I have to once again - and maybe for the millionth time since I started this blog - reiterate that Fed policy makes it a near-mathematical-impossibility for a soft landing for the economy. The flawed psychology of the last 2 decades of “buy the dip always”, fueled by dovish monetary policy and 0% interest rates, simply isn’t going to cut it with rates at 5% and the Fed tightening.

The entire playing field has changed, yet our psychology and sentiment toward the market has remained exactly the same. Something’s going to have to give. Does all of this sound familiar? I have been writing different versions of the same article for months now.

But make no mistake about it, I am choosing to start yet another week proclaiming the same message: the soft landing charade is exactly that - a charade. It’s a fallacy, nothing else, that remains alive and well in the ethos of finance and the financial media that, in my opinion, poses a sizeable current threat to markets at this point.

Have a look at this chart.