The Fed’s Balance Sheet Feeds Bailout Culture

"The question is whether they will be able to keep exercising discretion in the face of ever mounting federal debt and the increasing political pressure to purchase large quantities of that debt."

By Paul Mueller, American Institute For Economic Research

Fed-watching has become a hobby for many, and an occupation for some. When will the Fed cut interest rates? (September) How much will it cut interest rates? (25 – 50 basis points) How will this affect credit card and mortgage rates? (They will start coming down)

These are the kinds of questions most people ask. But what people wrongly ignore is the Fed’s huge balance sheet and its related consequences: subsidizing explosive government deficit spending and creating a bailout culture.

During the Global Financial Crisis of 2008, the Federal Reserve engaged in unprecedented interventions into the financial system. They opened Pandora’s Box and out of it came large scale asset purchase (LSAP) programs – better known as quantitative easing (QE). QE caused the Fed’s balance sheet to expand dramatically.

Quantitative easing allowed the Fed to expand its securities purchases into other asset markets besides US Treasuries – namely mortgage-backed securities (MBS). Although the first QE program was justified as a crisis measure, once the Fed crossed that line it would do so again and again for what could hardly be called emergencies. The legacy of quantitative easing continues to this day.

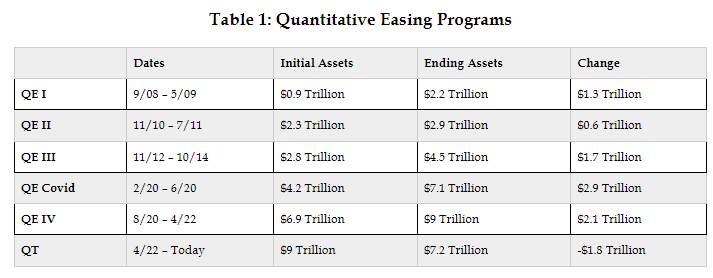

Let’s take a brief look at QE programs over the past fifteen years and speculate about what lies ahead. Table 1 shows five distinct periods of quantitative easing and their magnitudes. It also highlights the past two years of quantitative tightening.

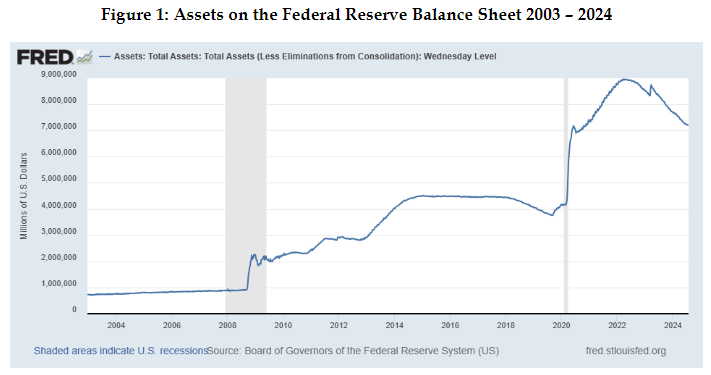

Figure 1 shows the effects of all this QE on the Fed’s balance sheet.

In November of 2008, financial markets around the world were distressed. In the US, stocks were down almost 50 percent from a year earlier. Bear Stearns had failed in March. Lehman had failed in September. American Insurance Group (AIG) had been bailed out not once but twice. Then Treasury Secretary Paulson had testified to Congress in late September that another great depression was imminent if they failed to authorize the $600 billion Troubled Asset Relief Program (TARP) to rescue the financial system.

Bernanke and the FOMC had been actively reducing the federal funds rate from 5.25 percent in August 2007 to less than .25 percent by December 2008. They had also launched a variety of temporary liquidity facilities to dampen the fire sale pressure on financial assets. By late 2008, their target interest rate was nearly at the zero lower bound, but they wanted to do more to shore up financial markets.

Quantitative Easing I

In November 2008 the Federal Reserve opted to create more liquidity using the Fed’s balance sheet. It announced that it would buy $600 billion of securities to provide more liquidity to the market. $100 billion would go towards buying “GSE direct obligations” or agency debt, and the other $500 billion would go towards buying MBS backed by GSEs.

But that was just the beginning.

In March of 2009, citing weakness in the economy, the Fed doubled down on this strategy. It announced that it would expand its bond-buying program in three ways. First, it authorized the purchase of an additional $750 billion in agency-backed MBS. Second, it authorized the purchase of up to another $100 billion of agency debt. Third, it authorized adding up to $300 billion in purchases of long-term Treasury bonds.

At the end of this bond-buying spree, known now as Quantitative Easing I (QEI), the Fed’s balance sheet stood at $2.3 trillion in June 2010 – a 200 percent increase from early 2008.

Graph 2: Federal Reserve Balance Sheet Assets 2008 – 2010

The Fed had provided massive liquidity to financial institutions and financial markets. But they had to figure out how to avoid an inflationary boom from that additional liquidity multiplying the money supply. To do this, the Fed utilized a new tool to “sterilize” all this new liquidity: interest on reserves (IOR). The Fed started paying banks interest on their reserves to encourage them to hold more reserves by issuing fewer new loans. The money supply (M1, M2, etc.) did not grow in nearly the same proportion as the monetary base did.

By late 2010, the FOMC indicated it would let its balance sheet shrink naturally as its assets matured and “rolled-off.” They estimated that their balance sheet would shrink back to $1.7 trillion by 2012. And so the first major foray into quantitative easing by the US ended with a whimper and with shifting goals more than a year and a half after the 2008 financial crisis.

Yet subsequent decades suggest that the Fed apparently had no interest in going back to pre-crisis levels. Though June 2010 was the end of QE I, it turns out QE I was only the opening overture of the Fed’s asset-buying spree of the past decade and a half.

Quantitative Easing II

Only a few months after indicating it would let assets start rolling off its balance sheet, the FOMC shifted course. With unemployment remaining stubbornly high throughout 2010, Bernanke and the FOMC decided to engage in another round of QE to put more liquidity in the economy. Although the financial crisis was well over by late 2010, the Fed still felt responsible for “fixing” the American economy – especially reducing the elevated unemployment rate. This would be its ever-weakening justification for buying huge quantities of securities whenever it felt like doing so.

This second round of QE involved buying another $600 billion of Treasury securities by the middle of 2011. By July 2011 when the Fed ended QE II, its balance sheet stood at roughly $2.8 trillion, half a trillion greater than its $2.3 trillion balance in 2010.

Quantitative Easing III

But as economies have a tendency of doing, the US economy did not respond to the half trillion purchase of Treasury securities the way Bernanke wanted. So in September 2012, Bernanke decided to pull out all the stops. He launched QE III or what some have called “QE-Infinity.” Under this third round of quantitative easing, the Fed began buying $40 billion of MBS every month. Within a few months they had increased their monthly purchases to $85 billion.

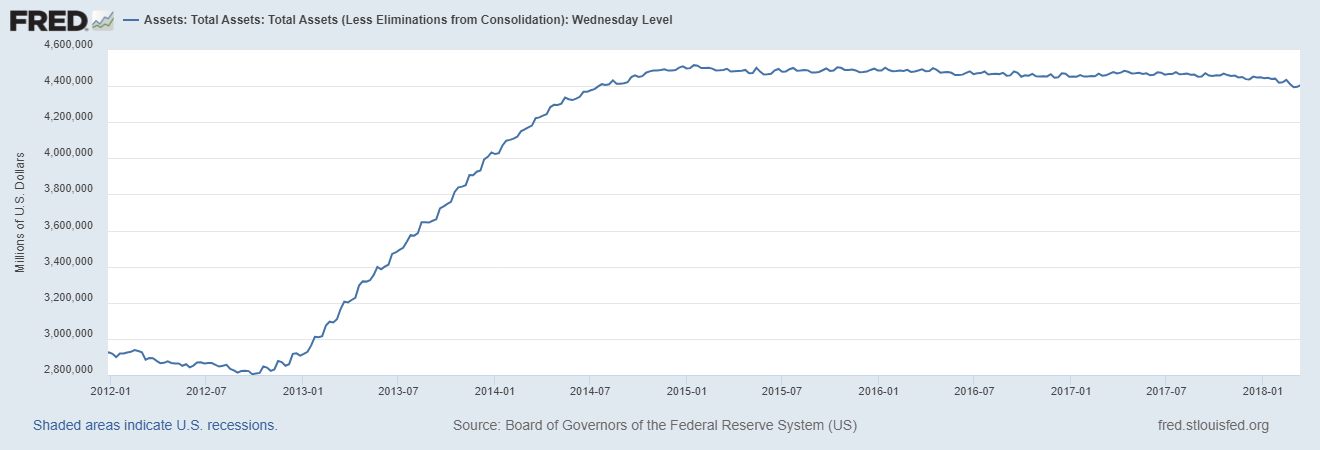

The program continued until October 2014, having begun tapering off their purchases in January 2014. By then the Fed’s balance sheet had grown almost two trillion dollars to $4.5 trillion. These numbers would have been unfathomable just a decade earlier.

Graph 3: Federal Reserve Asset Growth During QE III

Yet it appears that Fed officials came to believe that they had the authority and power to do whatever they deem necessary to “fix” the economy. That belief was on full display in the Fed’s response to the pandemic, their response to the Silicon Valley Bank and Signature Bank failures, and their recent tapering of the quantitative tightening program.

Quantitative Easing Covid

When the global pandemic took off in early 2020, the Federal Reserve didn’t miss a beat. With governments shutting down economic activity and millions of people dropping out of the labor force, the Fed promised to inject as much liquidity as it took to keep financial markets stable. It turns out that number was just shy of $3 trillion – injected over 3-4 months.

Quantitative Easing IV

In a surprisingly similar pattern to the post GFC world, the Federal Reserve abruptly stopped injecting liquidity and expanding its balance sheet in July of 2020 and even let it start shrinking again briefly. Yet, despite the worst of the pandemic being behind us, in August 2020 the Fed began another round of quantitative easing (QE IV) in which it would inject liquidity into the economy and expand its balance sheet for a year and a half and an additional $2 trillion.

Quantitative Tightening

In the wake of the Fed’s balance sheet exploding to nearly $9 trillion dollars, and the accompanying high inflation, in April of 2022 the Federal Reserve embarked on a significant round of quantitative tightening to reduce the size of its balance sheet. Since then, the Fed’s balance sheet has contracted by almost two trillion dollars. But as I’ve written elsewhere, they slowed their rate of QT in May to a trickle.

What Lies Ahead

We are on the cusp of a monetary loosening cycle. Market participants believe an interest rate cut in September is a done deal. More rate cuts will almost assuredly follow. The Fed will also announce relatively early in the rate-cutting cycle that they have reached an “ample reserve” level and will no longer allow their assets to roll off the balance sheet. And depending on economic conditions around employment levels and GDP growth, the Fed could very well start a new round of quantitative easing to supplement their interest rate cuts.

The Federal Reserve likes having a large balance sheet that they can expand or contract at will to massage financial markets. The open question is whether they will be able to keep exercising discretion in the face of ever mounting federal debt and the increasing political pressure to purchase large quantities of that debt.

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author. This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Interesting. Congress has the authority and the power to end all of this madness.

But they don’t, of course. All one needs to do to understand why is to examine the ‘balance sheets’ of 95% of Congressional members. Most of them enter Congress at least financially well off, compared to 90% of the population. And by the time they leave, they are in the 1%.

It’s such a massive scam.

It is the opinion of many of us that the Fed keeps more than one set of books. There is the one we are allowed to see as you describe in this article. But understanding the total debt in America today, both public and private, stands somewhere in the neighborhood of 100 Trillion Dollars, it becomes pretty clear the Fed has another set of books we will never see, as Bernanke once informed congress when asked by a representative, if they could audit the Fed's books. His short answer was NO, but if congress wished to withdraw the charter which authorized the creation of the Fed, they were free to do that. Of course congress is not going to do that, they would be jeopardizing their careers if they did, as the economy, which is hooked on cheap credit, would go into freefall, and most would blame congress for what would happen. Today America is held captive by the Fed and very few have the courage to challenge them. Congress could put the Dollar back on the gold standard, but again, that would hamper congress' ability to spend without worrying about paying for it.