Heed The Warning

Ignore short seller research if you want. Just don’t act surprised when it eventually reads like a prequel.

Last week served up another lesson on why short sellers should be read carefully, taken seriously, and provide immense benefit to investors and the market.

In case you missed it on Friday, Federal prosecutors in the Southern District of New York have charged individuals tied to Super Micro (SMCI) with orchestrating a scheme to illegally route billions of dollars’ worth of Nvidia-powered servers into China, in violation of U.S. export controls. The result, other than an arrest and board resignation, was SMCI stock getting porked royally, to the tune of -33.2% during Friday’s trading.

The stock is now down about -56% over the last 6 months.

According to the indictment, the accused allegedly worked together to bypass restrictions designed to prevent advanced AI hardware from reaching China without proper authorization—rules that are central to U.S. national security policy. Authorities have been increasingly focused on how such high-performance chips continue to make their way into China amid intensifying technological competition. One of the individuals named in the indictment is Wally Liaw, a co-founder and now-former board member of Super Micro Computer.

What makes this development particularly notable is that Liaw—and broader governance concerns at Super Micro—had already been highlighted by short sellers well before this indictment. In 2024, Hindenburg Research published a detailed report clearly laying out multiple red flags about Super Micro’s internal controls and decision-making. The lengthy report named Liaw in mutliple areas and alleges, in detail, “glaring accounting red flags, evidence of undisclosed related party transactions, sanctions and export control failures, and customer issues.”

It also noted that Liaw, who resigned in 2018 during an accounting controversy at the company, had been later rehired as a consultant in 2021 and ultimately reinstated to the board by 2023. Now, he’s been indicted.

I’m always a little stunned at how few people across the Street—buy side, sell side, and often even the companies themselves—actually read short reports in full. Not skim. Not glance at the headline. Actually read them. The best ones are not Twitter threads or vague hit pieces; they’re dense, footnoted, and built on primary evidence—contracts, filings, channel checks, and inconsistencies that require real work to uncover. You don’t have to agree with the conclusion, but dismissing them outright is intellectual laziness dressed up as conviction (and yes, I know, this is what the entire stock market is built on).

But at a minimum, any time a serious short seller publishes on a name you own, it should go straight to the top of your reading stack. Not because they’re always right—they’re not—but because they are often asking the exact questions management teams and bullish analysts are incentivized to avoid. The process of engaging with the short sellers’ findings forces a level of diligence that most investors simply don’t apply on their own.

Markets, of course, don’t always care right away about short sellers. In fact, more often than not, they don’t. Stocks can—and frequently do—shrug off detailed short reports in the near term, especially when the passive bid, options gamma, sentiment, momentum, or narrative are doing the heavy lifting. But time has a funny way of reconciling loose ends. Sometimes it takes quarters. Sometimes years. And sometimes, like we’re seeing here, it takes a federal indictment. The lag can be long and justice can be slow, but when it snaps back, it tends to do so violently.

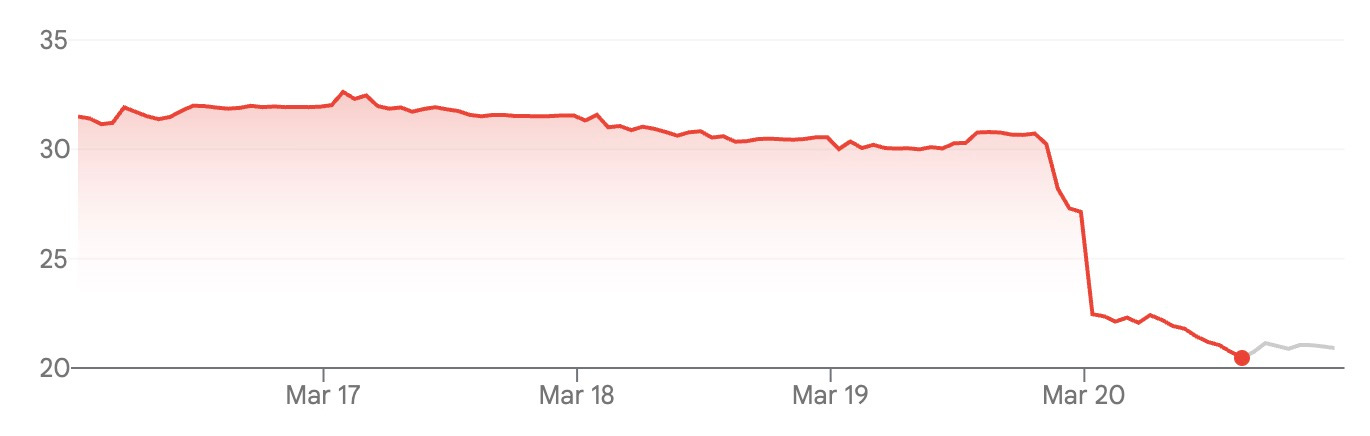

We’ve seen versions of this movie before. There are names where the debate dragged on endlessly while the stock levitated, like Herbalife. Its stock went from $60 to $5 over the course of five years, all but proving Bill Ackman’s short thesis.

But it was a pyrrhic victory. Massive capital was lost by Ackman during the years that he waged the war and ultimately he was forced out of the trade. But his thesis wasn’t wrong and the market eventually proved him right.

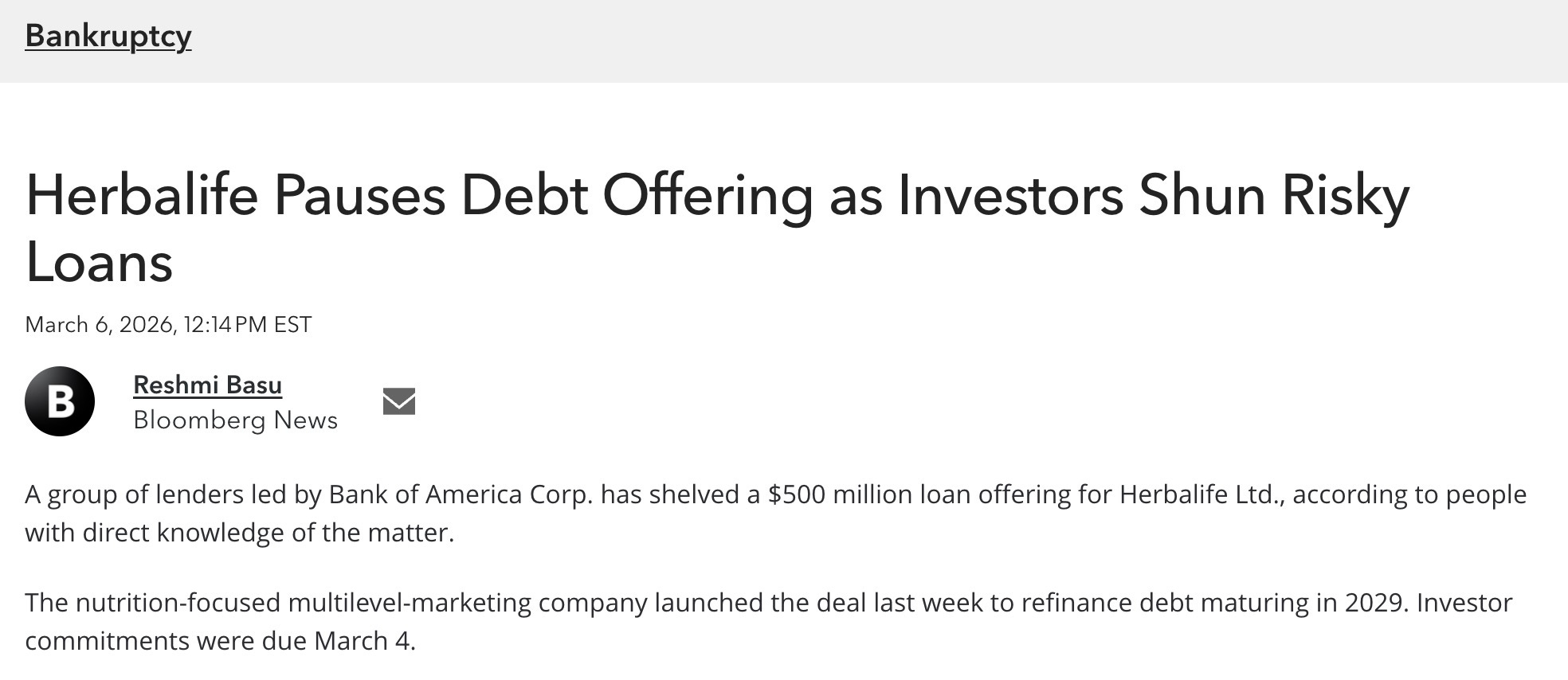

Now the company shows up in the “Bankruptcy” column on Bloomberg.

And so, like with Super Micro and Herbalife, whether you look at highly promotional growth stories, aggressive accounting situations, or governance red flags, the pattern is consistent: early warnings are often dismissed as “noise,” until they’re not.

That’s why I keep coming back to the idea that short sellers, at their best, function as a necessary counterweight in markets that otherwise skew toward optimism and narrative-building. They are one of the few groups economically incentivized to dig into what might be wrong, not just what could go right. That adversarial pressure is healthy. It sharpens price discovery. It forces better disclosure. And occasionally, it prevents outright fraud from going unchecked longer than it otherwise would.

It’s also worth remembering that many of the strongest short reports don’t hinge on a single “gotcha” moment. They’re mosaics—collections of smaller issues that, taken together, point to something structurally off. Weak controls. Questionable counterparties. Odd capital allocation decisions. Executive behavior that doesn’t quite pass the smell test. Any one of those can be explained away. All of them together? Much harder.

Which brings us to the present setup in a few other corners of the market. In at least one high-profile case, what I would consider a “smoking gun” has arguably already been laid out in plain sight. The work has been done. The receipts are there. And yet, as usual, it’s being largely ignored because the stock has held up and the story remains intact—for now. If history is any guide, that’s not a particularly durable defense.

And then just last week Muddy Waters recently published a critical report on SoFi, asking pointed questions the company wouldn’t answer and echoing broader concerns about the sustainability of BNPL and selling subprime loans, which is one of 10 areas of the market I personally believe are worth avoiding.

While the market reaction has been muted so far, the underlying thesis aligns with growing skepticism about credit quality and underwriting standards in a higher-rate environment. It also likely will get a negative tailwind from stress elsewhere in the market right now, private credit.

None of this is to say you should blindly follow short sellers. That’s just as dangerous as ignoring them. But treating their work as required reading—especially when it’s detailed, evidence-based, and persistent—is just basic risk management. You don’t get extra points for riding something all the way down because you refused to engage with opposing views.

The Super Micro situation is a reminder that the clock on these risks is often still ticking in the background. What appears irrelevant today can become central tomorrow, sometimes abruptly. Last week is also just another reminder that markets aren’t efficient, sell side analysts don’t give a fuck about you or the objective truth and the information edge in markets often isn’t about having access to something secret. It’s about taking seriously what’s already public—and having the discipline to read the stuff that makes you uncomfortable.

Or, put differently: you can ignore the short report if you want. Just don’t act surprised when it eventually reads like a prequel.

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Why would retail investors read short articles when they don't or can't read an annual report. Broad market ETF fund investing dosen't require a lot of brain activity. These investors believe they can hear something on X or YouTube buy it and the filthy lucre will roll in. Never understanding the difference between investing, trading or gambling.

I look at the posting about someone investing for 2 years learning about options.

Options are not investing. They are trading and so many trading in options are one click above degenerate gamblers.

I look back over the years since 1980 when I bought my first stock and how I have had my head and ass handed to me. I learned how to read annual reports, all the 10K stuff and releases. It is so much easier today to find information. My investing philosophy revolves around free cash flow and low P/E's. But that is just the start. I seldom look at short interest because most of the individual companies I invest in don't garner interest from short sellers.

To be fair, most of those reports are -at best- mental masturbation and at worst the Benjamin Button of pump and dumps.

In SCMIs case, treason is a pretty serious crime. My guess is that seizure is forthcoming alongside long walks in the prison yard with Bubba, Jerome and the entire butthole brigade.

Amat Victoria Curam.